UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission file number:

(Exact name of registrant as specified in its charter)

|

||

(State or other jurisdiction of incorporation) |

|

(I.R.S. Employer Identification No.) |

(Address of principal executive offices and zip code)

(

(Registrant’s telephone number, including area code)

Not Applicable

(Formed name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.:

Large accelerated filer |

|

☐ |

|

|

☒ |

|

Non-accelerated filer |

|

☐ |

|

Smaller reporting company |

|

|

Emerging Growth Company |

|

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Securities Act ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The aggregate market value of the registrant’s common equity held by non-affiliates of the registrant (assuming for purposes of this computation only that the directors and executive officers may be affiliates) at June 30, 2022, which was the last business day of the registrant’s most recently completed second fiscal quarter was approximately $

The number of outstanding shares of the registrant’s Class A common stock, par value $0.01 per share, and Class B common stock, par value $0.01 per share, as of February 25, 2023 were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2023 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year ended December 31, 2022.

Auditor Firm Id: |

Auditor Name: |

Auditor Location: |

|

|

|

|

|

Item 1. |

|

|

4 |

|

Item 1A. |

|

|

19 |

|

Item 1B. |

|

|

36 |

|

Item 2. |

|

|

36 |

|

Item 3. |

|

|

36 |

|

Item 4. |

|

|

36 |

|

|

|

|

|

|

Item 5. |

|

|

37 |

|

Item 6. |

|

|

37 |

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

38 |

Item 7A. |

|

|

58 |

|

Item 8. |

|

|

58 |

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

58 |

Item 9A. |

|

|

59 |

|

Item 9B. |

|

|

59 |

|

Item 9C. |

|

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections. |

|

59 |

|

|

|

|

|

Item 10. |

|

|

60 |

|

Item 11. |

|

|

60 |

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

60 |

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

60 |

Item 14. |

|

|

60 |

|

|

|

|

|

|

Item 15. |

|

|

61 |

|

Item 16 |

|

|

63 |

Except where the context requires otherwise and as otherwise set forth herein, in this report, references to the “Company”, “we”, “us” or “our” refer to Silvercrest Asset Management Group Inc. (“Silvercrest”) and its consolidated subsidiary, Silvercrest L.P., the managing member of our operating subsidiary (“Silvercrest L.P.” or “SLP”). SLP is a limited partnership whose existing limited partners are referred to in this report as “principals”.

Forward-Looking Statements

This report contains, and from time to time our management may make, forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, each as amended. For those statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to risks, uncertainties and assumptions. These statements are only predictions based on our current expectations and projections about future events. Important factors that could cause actual results, level of activity, performance or achievements to differ materially from those indicated by such forward-looking statements include but are not limited to: incurrence of net losses, fluctuations in quarterly and annual results, adverse economic or market conditions, our expectations with respect to future levels of assets under management, inflows and outflows, our ability to retain clients from whom we derive a substantial portion of our assets under management, our ability to maintain our fee structure, our particular choices with regard to investment strategies employed, our ability to hire and retain qualified investment professionals, the cost of complying with current and future regulation coupled with the cost of defending ourselves from related investigations or litigation, failure of our operational safeguards against breaches in data security, privacy, conflicts of interest or employee misconduct, our expected tax rate, and our expectations with respect to deferred tax assets, adverse effects of management focusing on implementation of a growth strategy, failure to develop and maintain the Silvercrest brand and other factors disclosed under “Risk Factors” in this annual report on Form 10-K. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

Summary Risk Factors

Our business is subject to risks of which you should be aware before making an investment decision. The risks described below are a summary of the principal risks associated with an investment in us and are not the only risks we face. These and other risks are discussed more fully in the section entitled “Risk Factors” in Part II, Item IA and elsewhere in this Annual Report on Form 10-K (our “Risk Factors”). Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business and the trading price of our securities.

Risks Related to our Investment Performance and the Financial Markets

Risks Related to our Key Professionals

Risks Related to our Growth

Risks Related to our Structure

Risk Related Generally to the Regulatory Environment in Which we Operate

Risks Related Generally to our Business

PART I.

Item 1. Description of Business.

Our Guiding Principles

We operate our business in accordance with the following guiding principles:

Our Company

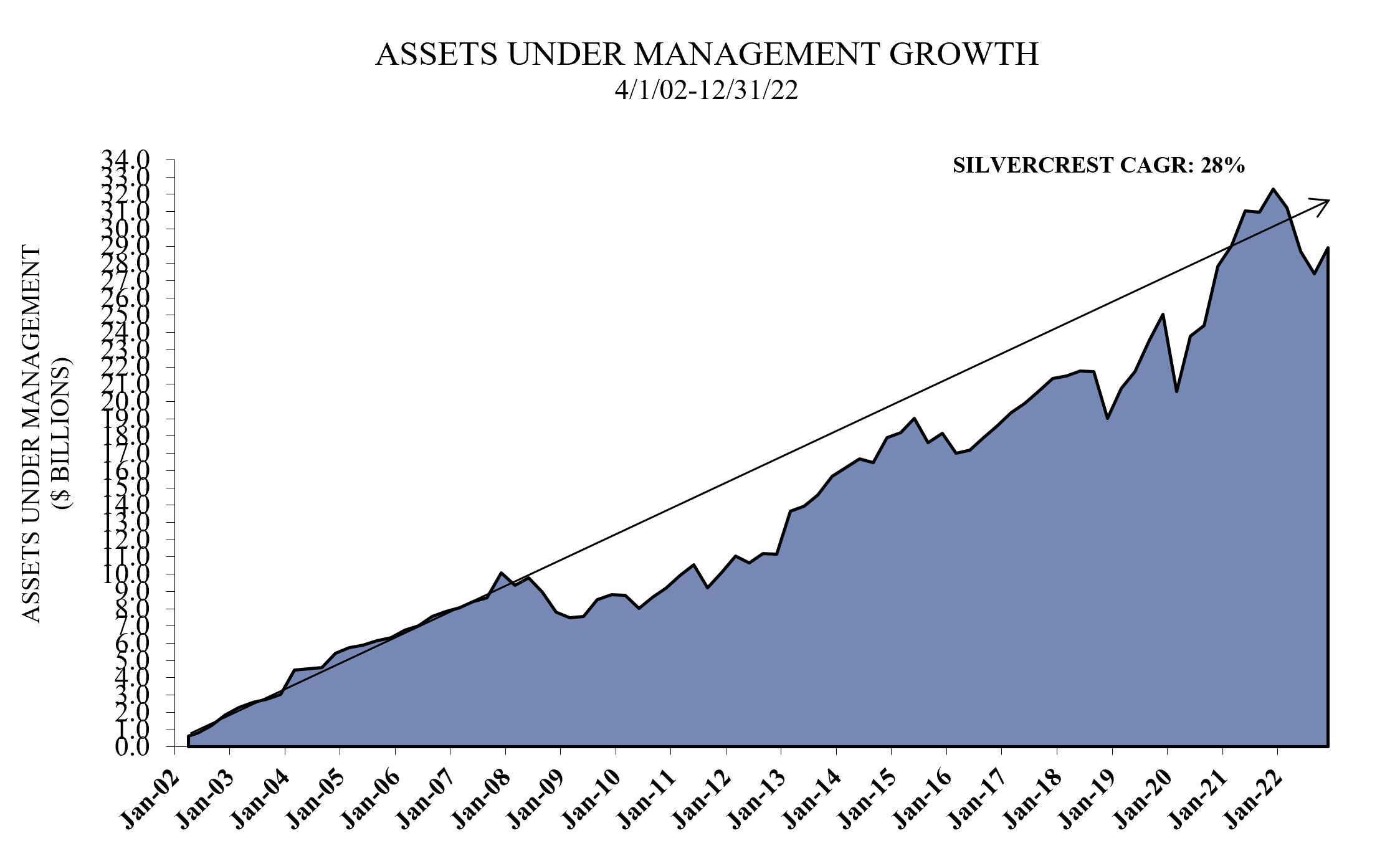

We are a full-service wealth management firm focused on providing financial advisory and related family office services to ultra-high net worth individuals and institutional investors. In addition to a wide range of investment capabilities, we offer a full suite of complementary and customized family office services for families seeking comprehensive oversight of their financial affairs. As of December 31, 2022, our assets under management were $28.9 billion.

We were founded 20 years ago on the premise that if we staffed and organized our business to deliver a combination of excellent investment performance together with high-touch client service, we would differentiate our business from a crowded field of firms nominally in the wealth management business. We seek to attract and serve a base of individuals and families with $10 million or more of investable assets, and we believe we are well-positioned to offer comprehensive investment and family office service solutions to families with over $25 million of investable assets. As of December 31, 2022, we had 841 client relationships with an average size of $34 million that represented approximately 99% of our assets under management. Our top 50 relationships averaged $349 million in size, and such amount represented approximately 60% of our assets under management. As a boutique, we are large enough to provide an array of comprehensive capabilities, yet agile enough to coordinate and deliver highly personalized client service.

Our annual client retention rate has averaged 98% since 2006 and, as shown below, the compound annual growth rate, or CAGR, in our assets under management since inception is 28%. Our growth rate in any 12-month period ending on the last day of a fiscal quarter since inception ranged from (23%) to 1,142%, with a mean of 34%. We believe our record of growth is a direct result of our demonstrated record of delivering excellent performance together with highly personalized service to our clients.

4

Our organic growth has been complemented by selective hiring and by nine successfully completed strategic acquisitions that have expanded not only assets under management, but also our professional ranks, geographic footprint and service capabilities. We believe additional acquisitions will allow us to extend our geographic presence nationally. As we grow, we will maintain our value proposition to continue to deliver to our clients excellent investment performance together with excellent client service, the essence of what differentiates us from our competitors.

Our clients engage us to advise them on traditional investment strategies focused on equities, fixed income and cash as well as non-traditional investment strategies including hedge funds, private equity funds, real estate and commodities. Our clients receive a full menu of proprietary investment capabilities together with a focused array of complementary non-proprietary capabilities offered by unaffiliated firms selected by us. In addition to our investment capabilities, we also provide our clients with family office services and related administrative services, which include financial planning, tax planning and preparation, partnership accounting and fund administration, and consolidated wealth reporting. Our fees for our investment advisory services, non-proprietary services and family office and related administrative services are structured to align our financial incentives with those of our clients to ensure they receive unconflicted advice. The vast majority of our fees are derived from discretionary assets under management, and are based on the value of the assets we manage for our clients. These fees increase if our clients’ assets grow in value; on the other hand, these fees decrease if our clients’ assets decline in value. Unlike our management fees, our fees for family office services and related administrative services are generally not based on or correlated to market values. For these services, we generally charge our clients a negotiated fee based on the scope of work. These services create strong client relationships and contribute meaningfully to our record of client retention.

As of December 31, 2022, approximately 68% of our discretionary assets under management were held for individual clients and 32% for institutional clients. Based on the results we have achieved in a number of our equity strategies, we continue to attract a significant amount of institutional investor interest. Our equity capabilities are on the approved lists of several prominent institutional consultants and, as a result, we believe significant institutional growth is likely to continue in future years.

5

History, Organization and Philosophy

When forming our company, our founders had the objective of creating a large full-service boutique operation focused on managing portfolios and delivering financial advice to wealthy individuals and select institutions. We commenced operations in April of 2002 as a corporation. Our first partners and employees came almost entirely from Donaldson, Lufkin & Jenrette (“DLJ”) Asset Management Group, which had been acquired by Credit Suisse Asset Management in late 2000. In 2002, we carefully recruited and hired the same equity, fixed income and client service teams with whom our clients had worked at DLJ Asset Management Group. As of December 31, 2022, approximately eight percent of our 154 employees are veterans of DLJ. Many of our principals, therefore, have worked together for 26 years and, in some cases, even longer.

On June 26, 2013, Silvercrest completed its corporate reorganization, and on July 2, 2013, Silvercrest closed its initial public offering. Prior to that date, Silvercrest was a private company.

Our headquarters are located in New York City with additional offices in Massachusetts, Virginia, New Jersey, California and Wisconsin. From inception, we have embraced an organizational structure in which the primary functions of client service, investments, technology and operations, and business administration are organized and staffed with professionals who specialize in each of those functions. This structure permits each professional to focus on his or her area of expertise without the distraction of other business responsibilities. At many other firms, the senior professionals are expected to serve multiple roles simultaneously, which we believe dilutes the value to clients and makes scaling the business effectively unachievable. We firmly believe that our business structure represents a better approach and will permit us to greatly expand our business on our existing platform.

To meet our primary objective to deliver strong investment results, we seek to add value through our asset allocation advice, as well as through our proprietary equity and fixed income strategies and outsourced investment capabilities. We recruited and hired a team of seasoned securities analysts who have an institutional caliber approach to security selection and a long record of success in implementing their strategies. We encourage them to focus 100% of their professional time on the task of securities selection. Our in-house growth and value equity analysts are focused on U.S. large cap, small cap, smid cap, multi cap, equity income and focused value equity strategies. On the fixed income side, our analysts are focused on high-grade municipals, high-yield municipals and high-grade taxables.

In order to deliver excellent client service, our portfolio managers are charged with the responsibility of working individually with each client to help define investment objectives, risk tolerance, cash flow requirements and other financial needs. Client-facing portfolio managers, their support staffs and the family office services group, account for 65% of our total employees, a reflection of our high commitment to excellent client service. We are staffed to ensure that each client receives senior level personal attention.

We have a staff of nine professionals who work with our portfolio managers to deliver family office services to interested clients. The fees for family office services are negotiated with the client and generally are not asset-based. For this reason, the revenues generated by our family office services are non-correlated to market movements and provide us with a diversified source of earnings. We believe these family office services have been an attractive component of our overall value proposition and engender a stronger relationship with our clients, leading to greater client retention and the institutionalization of client relationships.

Our Growth Strategy

We built our company to take market share from financial services firms whose wealth management models we believe are flawed. Our growth strategy has been and will continue to be to grow our business organically, to complement our organic growth with strategic hires and acquisitions and to expand our presence in the institutional market. In support of each of these initiatives we plan to continue to invest in establishing our brand through continued selective advertising and public relations.

Organic Growth

We have a proven ability to identify, attract and retain ultra-high net worth clients who seek a firm designed to deliver excellent investment performance and excellent client service. Our organizational model of separate and distinct business functions has proven scalable and our company’s assets under management have grown to $28.9 billion as of December 31, 2022 without a commensurate increase in headcount. Importantly, we have achieved our growth while maintaining our profitability during one of the most challenging periods in the history of the U.S. financial markets. Going forward, we will continue to execute our business plan for attracting ultra-high net worth clients.

6

The business of attracting ultra-high net worth clients is the business of obtaining referrals and gaining trust. At our company, these responsibilities reside principally with our portfolio managers. Our senior portfolio managers have on average nearly 41 years of industry experience and they have developed a wealth of contacts and professional referral sources as a result of that experience. In spearheading the effort to deliver excellent performance and service to their clients, our portfolio managers have developed very close relationships with their clients and in many cases these relationships are much older than our company itself. Much of our new business results from referrals from existing clients. In this regard, it is critical that our portfolio managers work closely with each of their clients to establish and maintain the trust that is at the heart of the relationship.

Where appropriate, our portfolio managers are also encouraged to introduce our clients to our family office services capabilities and we have capacity for growth in client utilization of these services. Five of our ten largest clients use our family office services and some of these clients have closed their own family offices to consolidate those activities with us. This is a profitable business for us and it serves to tighten our ties to those clients who avail themselves of the services we offer. It is also extremely useful to us in new business competitions where we use these services as a differentiator from our competitors. We continue to see the opportunity for greater penetration with our current clients in future years.

Complementing the efforts of our senior portfolio managers to cultivate client referrals, our business development team is charged with identifying newly-formed wealth (resulting from merger, acquisition or corporate finance) and then creating customized solicitations. Our objective is two-fold: we will expand awareness of our company and its capabilities by distributing our marketing materials to this new audience and we will attract a certain amount of new business. The basis of this effort is careful research designed to ascertain if the prospect has any relationship with us-or any of our clients or friends-and then our solicitation is tailored to those circumstances.

In all of our business development efforts we devote a great deal of time and effort to developing highly customized and detailed proposals for our prospects. In order to do so, we spend as much time as is required to thoroughly understand the prospect’s circumstances and goals as well as the sources of its dissatisfaction with its existing adviser. Where appropriate our proposals include the integration of our entire suite of family office services. We believe our customized new business presentations distinguish us from both our much larger competitors, which have substantial resources, but whose size, we believe, may impede them from easily tailoring solutions to suit clients’ needs, as well as from our smaller competitors which, we believe, do not have our depth of resources or capabilities.

Acquired Growth

From our inception, our organic growth has been complemented by selective hiring and strategic acquisitions, which have served to enlarge our client base, expand our professional ranks, increase our geographic presence and broaden our service capabilities. We therefore expect to continue to recruit and hire senior portfolio managers with significant client relationships as well as successful investment professionals with capabilities currently not available internally to us. We have used acquisitions to extend our presence into new geographies (Boston, Virginia, New Jersey, California and Wisconsin) and to gain new investment expertise. The nine strategic acquisitions we have successfully completed have allowed us to benefit from economies of scale and scope.

In making acquisitions, we look for firms with compatible professionals of the highest integrity who believe in our high service-high performance model for the business. It is important that their clientele be principally clients of high net worth and it is helpful if they have similar value and growth-based investment methodologies. These firms are attracted to our company by the strength of our brand, the breadth of our services and the integrity of our people. Often these firms are extremely limited in the investment products and services they can offer their clients and it is not uncommon that they have succession or other management issues to resolve. In addition, the high and growing cost of compliance with federal and state laws governing their business is often an added inducement. We believe we will become the partner of choice for many such firms.

To continue implementing our growth strategy, we intend to establish additional U.S. offices in major wealth centers on the West Coast, in the Southwest and in the Midwest in order to be closer to both our clients and to prospective clients.

Our past acquisitions have sharpened our ability to integrate acquired businesses, and we believe that once we identify an acquisition target we will be able to complete the acquisition and integrate the acquired business expeditiously.

Institutional Growth

After fourteen years of effort focused on cultivating relationships with institutional investment consultants, we continue to regularly make new business presentations to institutional investors, including public and corporate pension funds, endowments, foundations, and their consultants.

7

We are on the “approved” lists of certain prominent institutional investment consultants, which means that these consultants would be permitted to recommend our firm to institutional clients in search of a particular investment strategy for their clients. This has significantly enhanced our ability to win mandates that these consultants seek for their institutional clients and, as a result, we have won institutional mandates in our equity strategies. We expect this trend to continue once it is publicly known that these and other institutions have engaged us to manage significant portfolios for them. The importance of institutional growth to our company is noteworthy: institutional assets will likely expand not only our assets under management but also our profit margins; and the due diligence conducted by these institutions before selecting us will ratify and confirm the decisions to hire us made by our individual clients.

Over the past few years we have deliberately and gradually built our team and capability focused on providing Outsourced Chief Investment Officer services (“OCIO”). These services typically involve management on a discretionary or advisory basis for complex, multi-asset class pools of capital, often for tax exempt entities. On a discretionary engagement, our team provides a full-service approach inclusive of asset allocation, manager selection and due diligence, customized portfolio construction and risk analytics. On an advisory basis, these services can be performed without discretion or on a tailored basis. Traditionally, investment committees of these entities would manage the assets directly. However, with the growth in the size and complexity of many asset pools, these entities are often seeking outside management and advice.

Brand Management

We have invested heavily to build, maintain and extend our brand. We have done so in the belief that creating awareness of our company and its differentiated characteristics would support all aspects of our business, but most notably our growth.

With limited resources, we have created a focused national advertising campaign, which has drawn praise from clients, prospects and competitors alike. We have carefully chosen media outlets that reach our target audience efficiently. This effort has resulted in appearances on CNBC. We estimate that the new business that we get directly as a result of our advertising now finances its cost.

Complementing our advertising strategy, and again, with limited resources, we have also invested in an effort to get media coverage of our company in some of the nation’s most prestigious national publications as well as in industry journals and newsletters. This effort has resulted in press coverage by the Wall Street Journal, Barron’s, Bloomberg, the Financial Times and The New York Times as well as various trade publications distributed within our industry. This public relations effort has proven very helpful in establishing our company as a leader in our industry.

Our Business Model

We were founded in 2002 to provide independent investment advisory and related family office services to ultra-high net worth individuals and endowments, foundations and other institutional investors. To this end, we are structured to provide our clients with institutional-quality investment management advice and/or services with the superior level of service expected by wealthy individuals.

To provide this high level of service, we rely on portfolio management teams and our family office services team to provide objective, conflict-free investment management selection and a fully integrated, customized family-centric approach to wealth management. We believe the combination of comprehensive family office service, excellent investment capabilities and a high level of personal service allows us to take advantage of economies of scale to service the needs of our ultra-high net worth clients.

We have dedicated investment management teams tasked with successfully implementing their respective investment strategies. To increase the probability of success in meeting this objective, our analysts are not responsible for client interaction, management of our business, marketing or compliance oversight. This enables us to effectively serve ultra-high net worth clients as well as institutions that typically perform in-depth due diligence before selecting a manager.

Delivering Investment Performance

The Investment Policy & Strategy Group (“IPSG”), which is comprised of our chief strategist and several of our senior portfolio managers, is charged with the responsibility of adding value through asset allocation and manager selection. This is done through the use of our proprietary investment management by our internal analysts, and by those whom we believe are best-of-breed external managers.

8

The IPSG develops model asset allocations assuming differing levels of risk, liquidity and income tolerance as well as conducting outside manager due diligence. Our proprietary model portfolio structures are not merely a backward-looking, mechanical exercise based on the past performance of different asset classes. Instead, our IPSG overlays our judgment on the likely future performance of different asset classes in arriving at optimal portfolio structures. None of our dedicated investment analysts serves on this committee, which safeguards the independence of the IPSG’s recommendations.

Our portfolio managers are responsible for creating a customized investment program for each client based upon the IPSG’s work. An interactive dialogue ensures that each portfolio plan is based upon each client’s defined written objectives. Each client’s portfolio strategy takes into account that client’s risk tolerance, income and liquidity requirements as well as the effect of diversifying out of low-basis and/or sentimental holdings.

Historically, the IPSG has added value to our clients’ portfolios through asset allocation weightings and manager selection.

From inception, we have employed a system of peer group reviews to ensure that client portfolios have been constructed in a manner consistent with our best collective thinking. In annual peer group reviews, the asset allocation within each client portfolio is compared with such portfolio’s defined objectives and portfolios that are not fully aligned with the investment objective are then singled out for further review and discussion. Our objective is for all clients to receive our best thinking and for portfolio managers to manage portfolios consistently with our policy. As a combination of these various factors, the client relationship is with us and not merely with an individual at our company.

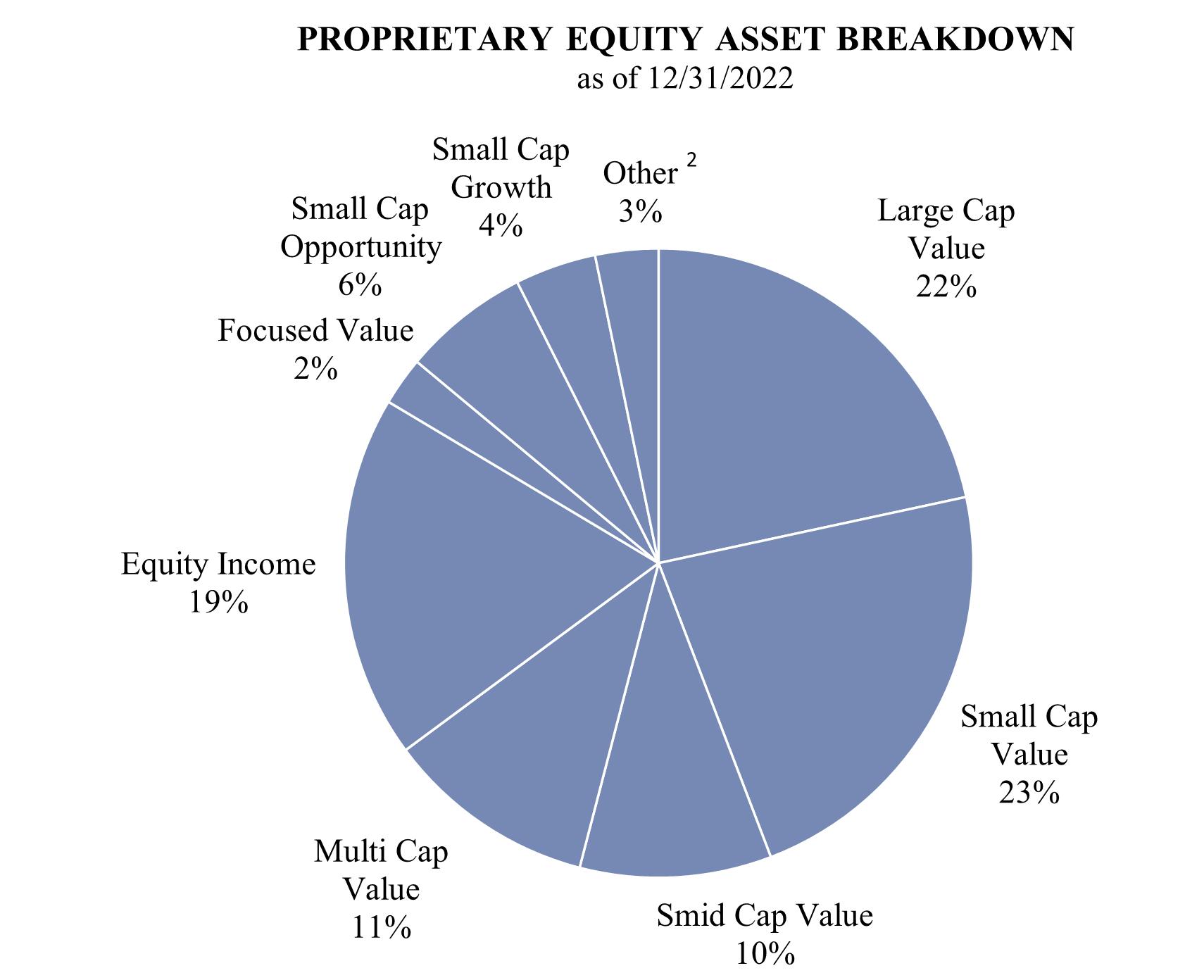

We believe that it is impossible for a single manager to perform all forms of investing equally well. Thus, our core proprietary investment capabilities are focused on a narrow range of highly disciplined U.S. equity and fixed income management strategies. Our investment teams have exhibited strong performance records. With respect to these strategies, roughly 61% of our total assets under management are managed in our proprietary investment strategies.

Our outsourced investment capabilities include alternative investments as well as traditional investment approaches in the categories of domestic large, mid and small cap growth equity, international equities and high-yield bonds.

Proprietary Equity Strategies

Our equity strategies rely on a team-based investment approach and a rigorous investment process. This approach has resulted in returns that exceed relevant market benchmarks. We believe this team approach has provided and will continue to provide consistency to our investment process and results over the long-term. Our investment analysts are generalists who employ a “bottom-up” equity selection methodology based upon their respective value, growth and international investment styles. Our analysts collectively monitor a universe of approximately 250 stocks that are deemed to be attractively valued relative to their business outlook and management’s history of creating shareholder value.

Once stocks have been approved for investment from this body of research, they become part of one or more model equity portfolios. These are generally large cap, small cap, smid cap, multi-cap, equity income and focused value. Each stock position is continually monitored against its investment thesis to ensure investment discipline, and, leveraging this discipline, we employ a strict policy to trim or sell securities in the following circumstances:

9

Below is a breakdown of assets among the various proprietary equity strategies as of December 31, 2022:1

_____________________________________________

10

Each of our equity strategies has outperformed its benchmark since inception as illustrated by the following chart:

PROPRIETARY EQUITY PERFORMANCE 1, 2 |

|

ANNUALIZED PERFORMANCE |

|

|||||||||||||||||||

AS OF 12/31/22 |

|

INCEPTION |

|

1-YEAR |

|

|

3-YEAR |

|

|

5-YEAR |

|

|

7-YEAR |

|

|

INCEPTION |

|

|||||

Large Cap Value Composite |

|

4/1/02 |

|

|

-11.6 |

|

|

|

8.3 |

|

|

|

9.0 |

|

|

|

12.0 |

|

|

|

9.2 |

|

Russell 1000 Value Index |

|

|

|

|

-7.5 |

|

|

|

6.0 |

|

|

|

6.7 |

|

|

|

9.1 |

|

|

|

7.4 |

|

Small Cap Value Composite |

|

4/1/02 |

|

|

-10.8 |

|

|

|

6.2 |

|

|

|

4.9 |

|

|

|

9.3 |

|

|

|

10.1 |

|

Russell 2000 Value Index |

|

|

|

|

-14.5 |

|

|

|

4.7 |

|

|

|

4.1 |

|

|

|

8.2 |

|

|

|

7.5 |

|

Smid Cap Value Composite |

|

10/1/05 |

|

|

-14.8 |

|

|

|

4.4 |

|

|

|

4.9 |

|

|

|

9.6 |

|

|

|

9.1 |

|

Russell 2500 Value Index |

|

|

|

|

-13.1 |

|

|

|

5.2 |

|

|

|

4.8 |

|

|

|

8.3 |

|

|

|

7.2 |

|

Multi Cap Value Composite |

|

7/1/02 |

|

|

-17.3 |

|

|

|

6.0 |

|

|

|

6.3 |

|

|

|

9.8 |

|

|

|

9.3 |

|

Russell 3000 Value Index |

|

|

|

|

-8.0 |

|

|

|

5.9 |

|

|

|

6.5 |

|

|

|

9.1 |

|

|

|

8.0 |

|

Equity Income Composite |

|

12/1/03 |

|

|

-7.3 |

|

|

|

5.4 |

|

|

|

6.9 |

|

|

|

10.9 |

|

|

|

11.0 |

|

Russell 3000 Value Index |

|

|

|

|

-8.0 |

|

|

|

5.9 |

|

|

|

6.5 |

|

|

|

9.1 |

|

|

|

8.1 |

|

Focused Value Composite |

|

9/1/04 |

|

|

-18.4 |

|

|

|

2.5 |

|

|

|

3.5 |

|

|

|

7.9 |

|

|

|

9.3 |

|

Russell 3000 Value Index |

|

|

|

|

-8.0 |

|

|

|

5.9 |

|

|

|

6.5 |

|

|

|

9.1 |

|

|

|

7.8 |

|

Small Cap Opportunity Composite |

|

7/1/04 |

|

|

-16.0 |

|

|

|

6.3 |

|

|

|

7.7 |

|

|

|

10.5 |

|

|

|

10.4 |

|

Russell 2000 Index |

|

|

|

|

-20.4 |

|

|

|

3.1 |

|

|

|

4.1 |

|

|

|

7.9 |

|

|

|

7.5 |

|

Small Cap Growth Composite |

|

7/1/04 |

|

|

-25.0 |

|

|

|

11.4 |

|

|

|

12.4 |

|

|

|

14.4 |

|

|

|

10.6 |

|

Russell 2000 Growth Index |

|

|

|

|

-26.4 |

|

|

|

0.6 |

|

|

|

3.5 |

|

|

|

7.1 |

|

|

|

7.6 |

|

Smid Cap Growth Composite |

|

1/1/06 |

|

|

-32.8 |

|

|

|

10.3 |

|

|

|

13.5 |

|

|

|

14.6 |

|

|

|

10.5 |

|

Russell 2500 Growth Index |

|

|

|

|

-26.2 |

|

|

|

2.9 |

|

|

|

6.0 |

|

|

|

9.0 |

|

|

|

8.7 |

|

11

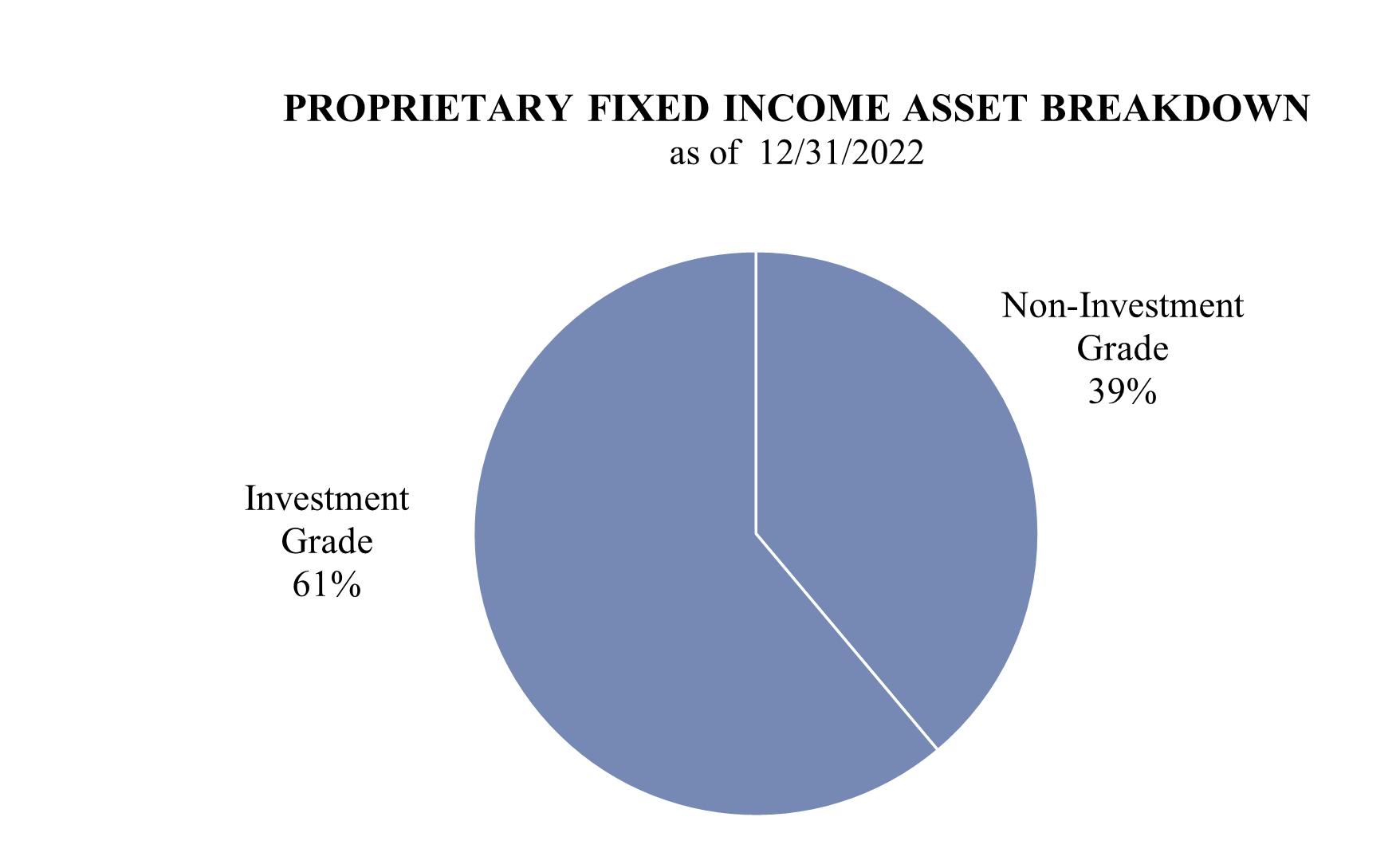

Proprietary Fixed Income Strategies

In the management of fixed income investments, clients typically give us the mandate to produce stable returns to dampen the volatility of their portfolios as a counter-weight to equities as part of their complete asset allocation. For those investors who can take advantage of the tax exemption of municipal bonds, we have developed two high-yield municipal bond products designed to add value to the returns possible from high-grade bonds in a low interest rate environment. Below is the breakdown of assets under management by strategy as of December 31, 2022:

Our fixed income strategy employs a bottom-up fundamental value approach designed to minimize the risk of loss. Almost all of our bond portfolios are highly customized and focused on income and liquidity generation as opposed to capital appreciation.

Outsourced Manager Selection

Recognizing the value of diversification to our clients, we offer a variety of outsourced investment capabilities designed to complement our proprietary capabilities. These outsourced capabilities include managers who have long records of success in managing growth equities, international equities, taxable high-yield bonds, hedge funds and other strategies not offered on a proprietary basis by us. In selecting these managers, we utilize an investment manager database for initial screening and then a dedicated staff conducts on-site due diligence. Potential managers are reviewed and selected by our IPSG. Our selection criteria include the following:

12

For large clients with significant hedge fund exposure, we offer a hedge fund advisory service that creates customized hedge fund portfolios. Each of our funds of funds appears below:

We have two types of fee arrangements with outsourced managers. Clients may either pay a discounted fee, negotiated by us, directly to the manager who retains the entire fee, or pay directly to the manager, who then distributes a portion of the fee to us. Clients are informed of the applicable arrangement and sign a written acknowledgement.

Delivering Client Service

We take a holistic approach to client service, whereby a senior portfolio manager spearheads the coordination of the IPSG recommendations, family office services work and the investment management team in order to deliver the full range of our capabilities to the client.

Four out of our ten largest high net worth clients use one or more components of our family office services. We believe that this is an attractive growth area for our company and we have initiated plans to increase the provision of these services to both broaden relationships with existing clients and to attract potential clients. Our family office services are profitable and are not used as a loss-leader for attracting clients. Our family office capabilities include the following:

For institutional client relationships, contact with our clients is handled by a dedicated institutional client service team headed by a Managing Director who also maintains our relationships with institutional investment consultants. This structure permits our investment professionals to maintain their focus on achieving superior investment results without the distraction of client demands.

Competition

The wealth management industry is highly competitive and is comprised of many players. We compete directly with some of the largest financial service companies, as well as some of the smallest. We primarily compete on the basis of several factors, including our level of service, the quality of our advice, independence, stability, performance results, breadth of our capabilities and fees. In general, these competitors fall into one of the following categories:

13

As a registered investment adviser that is not affiliated with other financial firms, we are free from the conflicts associated with brokerage or investment banking firms. In advising our clients on portfolio strategies, we are motivated to meet our clients’ investment objectives—not to generate commissions or placement fees—and to focus solely on providing excellent service and investment performance.

We have the size and resources to compete with larger organizations, and unlike many smaller firms, to provide our clients with fully customized, full-service wealth management and integrated family office solutions.

While many competitors outsource investment management, we have chosen to compete with excellent proprietary investment capabilities coupled with a focused array of complementary non-proprietary capabilities offered by unaffiliated firms. This combination enables us to compete for and win the business of wealthy investors. We believe this is a key to our past and future success.

Employees

As of December 31, 2022, we had 152 full-time employees and two part-time employees. None of our employees are subject to a collective bargaining agreement. We believe that relations with our employees continue to remain strong.

We are a full-service wealth management firm and our most important resources are our employees. We have a long history of low employee turnover which is directly the result of a culture that embraces an organizational structure in which the primary functions of client service, investments, technology, operations, and business administration are organized and staffed with professionals who specialize in each of those functions. This structure permits each professional to focus on his or her area of expertise without the distraction of other business responsibilities.

We attract talented individuals who share our entrepreneurial spirit and embrace our culture which is focused on delivering a combination of excellent investment performance together with high-touch client service.

Employees have opportunities for promotion either within their specific discipline or by joining other groups within the firm. We have also gained expertise in several disciplines as a result of acquisitions that we have completed which has resulted in filling necessary roles within the firm. Furthermore, several employees have been promoted to partner throughout our history.

Our firm also provides employees with opportunities to become members of various committees covering many disciplines including technology, operations and the Silvercrest Academy which provides internal professional development to all members of the firm. Many of our younger employees are provided the opportunity to take on leadership roles in the aforementioned committees as part of their own professional development. This allows employees to participate in firm advancement and encourages further collaboration throughout Silvercrest.

We also offer employees tuition assistance in order to support their educational aspirations and development within the firm.

Our employees and culture differentiate Silvercrest from other firms in the wealth management space and we will continue to attract and develop talent necessary to ultimately deliver on the promise of providing exceptional service to our clients and colleagues.

Our Structure and Reorganization

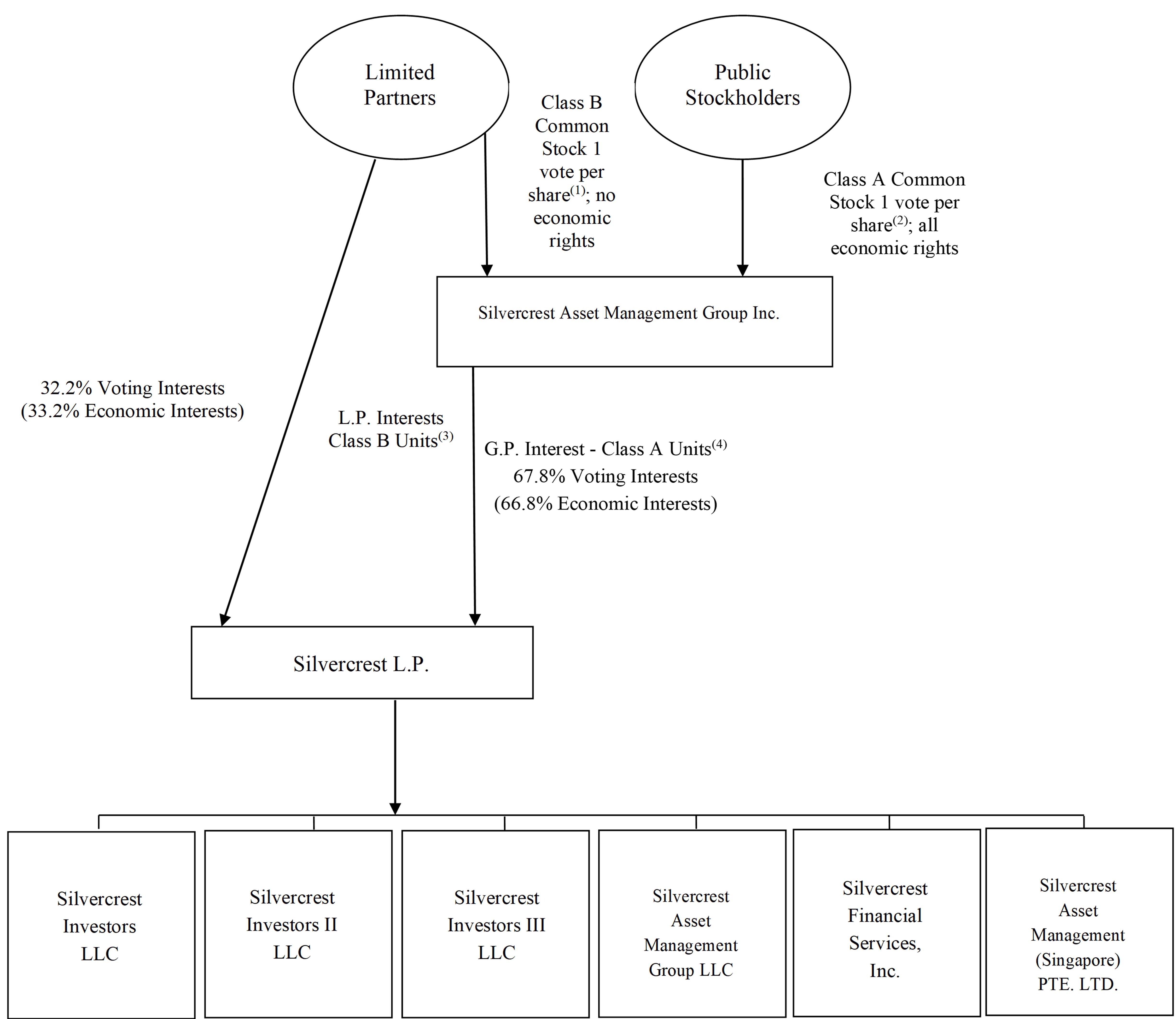

Holding Company Structure

Our only business is acting as the general partner of Silvercrest L.P. and, as such, we will continue to operate and control all of its business and affairs and consolidate its financial results into our financial statements. The ownership interests of holders of limited partnership interests of Silvercrest L.P. are accounted for as a non-controlling interest in our consolidated financial statements.

Net profits, net losses and distributions of Silvercrest L.P. are allocated and made to each of its partners on a pro rata basis in accordance with the number of partnership units of Silvercrest L.P. held by each of them. In addition, Silvercrest L.P. has issued deferred equity units and restricted stock units exercisable for Class B units that entitle the holders thereof to receive distributions from Silvercrest L.P. to the same extent as if the underlying Class B units were outstanding.

14

Set forth below is our holding company structure and ownership as of December 31, 2022.

15

Regulatory Environment

Our business is subject to extensive regulation in the United States at the federal level and, to a lesser extent, the state level. Under these laws and regulations, agencies that regulate investment advisers have broad administrative powers, including the power to limit, restrict or prohibit an investment adviser from carrying on its business in the event that it fails to comply with such laws and regulations. Possible sanctions that may be imposed include the suspension of individual employees, limitations on engaging in certain lines of business for specified periods of time, revocation of investment adviser license and other registrations, censures and fines.

The legislative and regulatory environment in which we operate has undergone significant changes in recent years. New laws or regulations, or changes in the enforcement of existing laws or regulations, applicable to us, our activities and our clients may adversely affect our business. Our ability to function in this environment will depend on our ability to monitor and promptly react to legislative and regulatory changes. There have been a number of highly publicized regulatory inquiries that have focused on the investment management industry. These inquiries have resulted in increased scrutiny of the industry and new rules and regulations for investment advisers. This regulatory scrutiny may limit our ability to engage in certain activities that might be beneficial to our stockholders.

In addition, as a result of market events, acts of serious fraud in the investment management industry and perceived lapses in regulatory oversight, U.S. and non-U.S. governmental and regulatory authorities may increase regulatory oversight of our businesses. We may be adversely affected as a result of new or revised legislation or regulations imposed by the Securities and Exchange Commission (the “SEC”), the U.S. Commodity Futures Trading Commission (the “CFTC”), other U.S. or non-U.S. regulatory authorities or self-regulatory organizations that supervise the financial markets. We also may be adversely affected by changes in the interpretation or enforcement of existing laws and rules by these governmental authorities and self-regulatory organizations, as well as by U.S. and non-U.S. courts. It is impossible to determine the extent of the impact of any new proposed laws, regulations or initiatives that could apply to markets in which we trade, or whether any of those proposals will become law. Compliance with any new laws or regulations could add to our compliance burden and costs and affect the manner in which we conduct our business.

SEC Regulation

SAMG LLC is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). The Advisers Act, together with the SEC’s regulations and interpretations thereunder, imposes substantive and material restrictions and requirements on the operations of investment advisers. The SEC is authorized to institute proceedings and impose sanctions for violations of the Advisers Act, ranging from fines and censures to termination of an adviser’s registration.

The Advisers Act imposes substantive regulation on virtually all aspects of our business and relationships with our clients. As a registered investment adviser, we are subject to many requirements that cover, among other things, disclosure of information about our business to clients; maintenance of written policies and procedures; maintenance of extensive books and records; restrictions on the types of fees we may charge, including performance fees; solicitation arrangements; engaging in transactions with clients; maintaining an effective compliance program; custody of client assets; client privacy; advertising; pay-to-play; cybersecurity and proxy voting. The SEC has authority to inspect any registered investment adviser from time to time to determine whether the adviser is conducting its activities (i) in accordance with applicable laws, (ii) consistent with disclosures made to clients and (iii) with adequate systems and procedures to ensure compliance.

16

As an investment adviser, we have a fiduciary duty to our clients. The SEC has interpreted this duty to impose standards, requirements, and limitations on, among other things: trading for proprietary, personal and client accounts; allocations of investment opportunities among clients; use of soft dollars; execution of transactions; and recommendations to clients. We manage 88% of our accounts on a discretionary basis, with authority to buy and sell securities for each portfolio, select broker-dealers to execute trades and negotiate brokerage commission rates. In connection with these transactions, we receive soft dollar credits from broker-dealers that have the effect of reducing certain of our expenses. Section 28(e) of the Securities Exchange Act of 1934, or the Exchange Act, provides a “safe harbor” to an investment adviser against claims that it breached its fiduciary duty under state or federal law (including The Employee Retirement Income Security Act of 1974, as amended, or ERISA) solely because the adviser caused its clients’ accounts to pay more than the lowest available commission for executing a securities trade in return for brokerage and research services. To rely on the safe harbor offered by Section 28(e), (i) we must make a good-faith determination that the amount of commissions is reasonable in relation to the value of the brokerage and research services being received and (ii) the brokerage and research services must provide lawful and appropriate assistance to us in carrying out our investment decision-making responsibilities. In permissible circumstances, we may receive technology-based research, market quotation and/or market survey services which are paid for in whole or in part by soft dollar brokerage arrangements. If our ability to use soft dollars were reduced or eliminated as a result of the implementation of statutory amendments or new regulations, our operating expenses would increase.

Under the Advisers Act, our investment management agreements may not be assigned without client consent. The term “assignment” is broadly defined and includes direct assignments as well as assignments that may be deemed to occur upon the transfer, directly or indirectly, of a controlling interest in an investment adviser.

The failure of SAMG LLC to comply with the requirements of the Advisers Act, and the regulations and interpretations thereunder, could have a material adverse effect on us.

Dodd-Frank

The Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, was signed into law on July 21, 2010. The Dodd-Frank Act has not caused us to reconsider our basic strategy. However, certain provisions have, and others may continue to increase regulatory burdens related to compliance costs. The scope of many provisions of the Dodd-Frank Act has been, or will be, determined by implementing regulations, some of which will require lengthy proposal and promulgation periods.

The Dodd-Frank Act affects a broad range of market participants with whom we interact or may interact. Regulatory changes that will affect other market participants are likely to change the way in which we conduct business with our counterparties. Although many aspects of the Dodd-Frank Act have been implemented, there remains significant uncertainty regarding implementation of other aspects of the Dodd-Frank Act. While its impact on the investment management industry and us cannot be predicted at this time, it will continue to be a risk for our business.

ERISA-Related Regulation

To the extent that SAMG LLC or any other of our affiliates acts as or is considered to be a “fiduciary” under ERISA or similar laws with respect to benefit plan clients (including IRAs), SAMG LLC or the applicable affiliate is subject to certain applicable provisions of ERISA (and/or applicable provisions of the Internal Revenue Code of 1986, as amended, referred to as the Internal Revenue Code) and to regulations promulgated thereunder. Among other things, ERISA and applicable provisions of the Internal Revenue Code impose certain duties on persons who act as or who are considered to be fiduciaries under ERISA, prohibit certain transactions involving benefit plan clients and provide monetary penalties and taxes for violations of these prohibitions. Our failure to comply with these requirements could have a material adverse effect on our business.

Other Jurisdictions

Many countries other than the United States have enacted laws, rules, and regulations that apply to investment advisers and private fund managers that offer their services in those jurisdictions. Though it has client relationships with individuals who reside in jurisdictions other than the United States, Silvercrest does not market or offer its services in any jurisdiction other than the United States. Similarly, revisions to the EU’s Markets in Financial Instruments Directive (MiFID II), which took effect in January 2018, introduced new requirements for certain non-EU portfolio managers who provide certain investment services to EU investors. Should SAMG LLC or any of our other affiliates provide such services in the EU, it and such funds may be subject to the regulatory requirements of MiFID II.

17

In addition, we and/or our affiliates may become subject to additional regulatory demands in the future to the extent we expand our investment advisory business in existing and new jurisdictions. There are also a number of pending or recently enacted legislative and regulatory initiatives in the United States and in other jurisdictions that could significantly impact our business.

Compliance

Our legal and compliance functions are integrated into a team of professionals. This group is responsible for all legal and regulatory compliance matters, as well as monitoring adherence to client investment guidelines. Senior management is involved at various levels in all of these functions.

Available Information

We maintain a website at http://ir.silvercrestgroup.com/. We provide access to our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports free of charge through this website as soon as reasonably practicable after such material is electronically filed with the SEC. Paper copies of annual and periodic reports filed with the SEC may be obtained free of charge upon written request by contacting our headquarters at the address located on the front cover of this report or under Investor Relations on our website. In addition, our Corporate Governance Guidelines, Code of Business Conduct and Ethics, By-Laws, Audit Committee Charter, Compensation Committee Charter and Nominating and Governance Committee Charter are available on our website (under Corporate Governance) and are available in print without charge to any stockholder requesting them. The SEC maintains a website that contains reports, information statements, and other information regarding issuers like us who file electronically with the SEC. The SEC’s website is located at www.sec.gov.

18

Item 1A. Risk Factors.

Risks Related to our Investment Performance and the Financial Markets

Volatile market conditions could adversely affect our business in many ways, including by reducing the value of our assets under management and causing clients to withdraw funds, either of which could materially reduce our revenues, adversely affect our financial condition and earnings, and expose us to litigation risks.

The fees we earn under our investment management agreements with clients are based on the value of our assets under management. The prices of the securities held in the portfolios we manage and, therefore, our assets under management, may decline due to any number of factors beyond our control, including, among others, a declining stock or bond market, general economic downturn, political uncertainty, natural disasters or pandemics (including the most recent coronavirus outbreak), acts of terrorism or other catastrophic or geopolitical events. In periods of difficult market conditions, we may experience accelerated client redemptions or withdrawals if clients move assets to investments they perceive as offering greater opportunity or lower risk, which could further reduce our assets under management in addition to market depreciation. The economic outlook remains uncertain and we continue to operate in a challenging business environment. If market conditions, or actions taken by clients in response to market conditions, cause a decline in our assets under management, it would result in lower investment management fees and other revenue. If our revenues decline without a commensurate reduction in our expenses, our net income will be reduced, and our business will be negatively affected. In addition, while we seek to deliver long-term value to our clients, volatility may lead to under-performance in the near term, which could adversely affect our results of operations.

If market conditions improve greatly, driving the prices of the securities in our clients’ accounts higher, it may lead to withdrawals or redemptions. In many cases, we advise only a portion of our clients’ complete financial portfolio. This is because many clients prefer to diversify their portfolio among more than one asset manager or investment type. As to those clients, if the portion of their portfolio held by us increases significantly, it may become too large a percentage of their overall portfolio, and they may withdraw assets from our management and invest it elsewhere, thereby rebalancing their overall portfolio and returning their allocation to us to its prior level.

The performance of our investment strategies is critical to retaining existing client assets and to attracting new client assets. Our investment strategies may perform poorly for various reasons, including general market conditions, our investment decisions, and the performance of the companies in which we invest on our clients’ behalf. If our investment strategies perform poorly, on an absolute basis or relative to other investment advisers, or if the rankings of mutual funds we sub-advise decline, our clients may withdraw funds or terminate their relationships with us and investors in the mutual funds we sub-advise may redeem their investments, which may cause the revenues that we generate from investment management and other fees to decline. Further, third-party financial intermediaries, advisers, or consultants may rate our investment products poorly, which may lead our existing clients to withdraw funds from our investment strategies or reduce asset inflows from these third parties or their clients.

While clients do not generally have legal recourse against us due to poor investment results, if our investment strategies perform poorly, we are more likely to be subject to litigation brought by dissatisfied clients. In addition, if clients are successful in claiming that their losses resulted from fraud, gross negligence, willful misconduct, breach of contract or other similar misconduct, these clients may have remedies against us and/or our investment professionals under the federal securities laws and/or state law.

We may not be able to maintain our current fee structure as a result of poor investment performance, competitive pressures or as a result of changes in our business mix, which could have a material adverse effect on our profit margins and results of operations.

In recent years, there has been a general trend toward lower fees in the investment management industry. Some of our investment strategies, because they tend to invest in larger-capitalization companies and are designed with larger capacity and to appeal to larger clients, have lower fee schedules. In order to maintain our fee structure in a competitive environment, we must be able to continue to provide investment returns and service that our clients believe justify our fees. If our investment strategies perform poorly, we may be forced to lower our fees in order to retain and attract assets to manage. Furthermore, if an increased part of our assets under management are invested in our larger capacity, lower fee strategies, our revenue could be adversely affected.

19

The historical returns of our existing investment strategies may not be indicative of future results or of future results of investment strategies that we may develop.

We have outlined the historical returns of our existing investment strategies under the “Business” heading in this report. The historical returns of our strategies should not be considered indicative of the future results of these strategies or of the results of any other strategies that we may develop in the future. The investment performance we achieve for our clients varies over time and the variance can be wide. The historical performance presented herein is as of December 31, 2022 and for the period then ended. The performance we achieve as of a subsequent date and for a subsequent period may be higher or lower and the difference may be material. Our strategies’ returns have benefited during some periods from investment opportunities and positive economic and market conditions. In certain periods, general economic and market conditions have negatively affected investment opportunities and our strategies’ returns. These negative conditions may occur again, and in the future, we may not be able to identify and invest in profitable investment opportunities within our current or future strategies.

We derive a substantial portion of our revenues from a limited number of strategies and clients.

As of December 31, 2022, $20.5 billion of our assets under management were concentrated in discretionary managed accounts, and the revenue from these discretionary managed accounts represented approximately 96% of our investment management fees for the twelve months ended December 31, 2022. In addition, $0.4 billion of our assets under management were invested in private partnerships as of December 31, 2022, and the revenue from these private partnerships represented approximately 4% of our investment management fees for the twelve months ended December 31, 2022. As a result, a substantial portion of our operating results depends upon the performance of a limited number of investment strategies used to manage those discretionary managed accounts and private partnerships, and our ability to retain client assets. If a significant portion of the investors in our larger strategies withdrew their investments or terminated their investment management agreements for any reason, including poor investment performance or adverse market conditions, our revenues from those strategies would decline, which would have a material adverse effect on our results of operations and financial condition.

Furthermore, certain of our strategies may derive a significant portion of their total assets under management from assets of a single client or a small number of clients. If any such clients withdraw all or a portion of their assets under management, our business would be significantly affected, which would negatively impact our investment management fees and could have a material adverse effect on our results of operations and financial condition.

Substantially all of our revenue generating contracts and relationships may be terminated upon no notice.

We derive our revenues principally from our assets under management, which may be reduced by our clients, or investors in the mutual funds we sub-advise, at any time. Any client may reallocate all or a portion of their assets under management with us at any time, on little to no notice. In addition, investors in the mutual funds we advise can redeem their investments in those funds at any time without prior notice. Further, our investment management agreements may be terminated or not renewed by our clients upon short notice or no notice, for any reason. The decrease in revenues that could result from a reduction in assets under management or the termination of a material client relationship or group of client relationships could have a material adverse effect on our business.

Our long-only, equity investment focus may not obtain attractive returns in the short-term or during certain market periods and may expose us to greater risk than if our investment strategies included non-equity securities or hedged positions.

Even when securities prices are rising generally, portfolio performance may be affected by our investment approach. Our investment strategies employ a long-term investment approach, which has outperformed the market in some economic and market environments and underperformed it in others. A prolonged period in which the growth style of investing outperforms the value style may cause portions of our investment strategy to go out of favor with some clients, consultants, or third-party intermediaries. Poor performance relative to peers, coupled with changes in personnel, unfavorable market environments or other difficulties may result in significant withdrawals of client or investor assets, client or investor departures or otherwise result in a reduction in our assets under management.

Our products are best suited for investors with long-term investment horizons. In order for our classic value investment approach to yield attractive returns, we must typically hold securities for an average of over three years. Therefore, our investment strategies may not perform well during short periods of time. In addition, our strategies may not perform well during points in the economic cycle when value-oriented stocks are relatively less attractive. For instance, during the late stages of an economic cycle or during periods where the markets are focused on one investment thesis or sector, investors may purchase relatively expensive stocks in order to obtain access to above average growth, as was the case in the late 1990s.

20

Our largest equity investment strategies hold long positions in publicly traded equity securities of companies across a wide range of market capitalizations, geographies and industries. Accordingly, when there is a general decline in the value of equity securities, each of our equity strategies is likely to perform poorly on an absolute basis. Aside from our privately managed funds and funds of funds, we do not have strategies that invest in privately held companies or take short positions in equity securities, which could offset some of the poor performance of our long-only, equity strategies. Even if our investment performance remains strong during declining market conditions relative to other long-only, equity strategies, investors may withdraw assets from our management or allocate a larger portion of their assets to non-long-only or non-equity strategies. In addition, the prices of equity securities may fluctuate more widely than the prices of other types of securities, making the level of our assets under management and related revenues more volatile.

The performance of our investment strategies or the growth of our assets under management may be constrained by the unavailability of appropriate investment opportunities.

Our investment performance depends in large part on our investment teams’ ability to identify appropriate investment opportunities. If any of our investment teams are unable to timely identify sufficiently appropriate investment opportunities for existing and new client assets, the investment performance of the relevant investment strategy could be adversely affected. In addition, if we determine that there are insufficient investment opportunities available for a strategy, we may restrict the strategy’s growth by closing the strategy to all or substantially all new investors or otherwise taking action to limit the flow of assets into the strategy. If we misjudge the point at which it would be optimal to limit access to or close a strategy, the strategy’s investment performance could be negatively impacted. The availability of sufficiently appropriate investment opportunities is influenced by a number of factors, including general market conditions. The risk that such opportunities may be unavailable is particularly acute with respect to our small cap and smid cap strategies that focus on small-cap investments, and is likely to increase as our assets under management increase, particularly if these increases occur very rapidly. If we are unable to identify appropriate investment opportunities, our growth and results of operations may be negatively affected. As of the filing of this annual report, our small cap value strategy is closed to new investors. The strategy may be reopened if one or more of our investors elects to rebalance its assets, which may occur at any time.

Our investment process requires us to conduct extensive fundamental research on any company before investing in it, which may result in missed investment opportunities and reduce the performance of our investment strategies.

Before we add any security to our portfolio, we undergo an in-depth research process, which takes a considerable amount of time, in order to understand the company and the business well enough to make an informed decision as to whether we are willing to own a significant position in a company, whose current earnings are below its historic norms and that does not yet have earnings visibility. However, the time we take to make this judgment may cause us to miss the opportunity to invest in a company that has a sharp and rapid earnings recovery. Any such missed investment opportunity could adversely impact the performance of our investment strategies.

Our International Equity Strategies invest principally in the securities of non-U.S. companies, which involve foreign currency exchange, tax, political, social and economic uncertainties and risks.

As of December 31, 2022, our international equity strategies, which invest primarily in companies domiciled outside of the United States, accounted for approximately 0.9% of our assets under management. In addition, some of our other strategies also invest on a more limited basis in securities of non-U.S. companies. Fluctuations in foreign currency exchange rates could negatively affect the returns of our clients who are invested in these strategies. In addition, an increase in the value of the U.S. dollar relative to non-U.S. currencies is likely to result in a decrease in the U.S. dollar value of our assets under management, which, in turn, could result in lower revenue since we report our financial results in U.S. dollars.

Investments in non-U.S. issuers may also be affected by tax positions taken in countries or regions in which we are invested, as well as political, social and economic uncertainty, particularly as a result of the recent decline in economic conditions. Declining tax revenues may cause governments to assert their ability to tax the local gains and/or income of foreign investors (including our clients), which could adversely affect clients’ interests in investing outside the United States. Many financial markets are not as developed, or as efficient, as the U.S. financial markets, and, as a result, those markets may have limited liquidity and higher price volatility. Liquidity also may be adversely affected by political or economic events within a particular country, and our ability to dispose of an investment also may be adversely affected if we increase the size of our investments in smaller non-U.S. issuers. Non-U.S. legal and regulatory environments, including financial accounting standards and practices, also may be different, and there may be less publicly available information about such companies. These risks could adversely affect the performance of our International Equity Strategies and may be particularly acute in the emerging or less developed markets in which we invest.

21

Risks Related to Our Growth

Our efforts to establish new investment teams and strategies may be unsuccessful and could negatively impact our results of operations and our reputation.

As part of our growth strategy, we may seek to take advantage of opportunities to add new investment teams. To the extent we are unable to recruit and retain investment teams that complement our business model, we may not successfully diversify our investment strategies and client assets, which could have a material adverse effect on our business and future prospects. In addition, the costs associated with establishing a new team and investment strategy initially will exceed the revenues they generate. If any such new strategies perform poorly or fail to attract sufficient assets to manage, our results of operations and reputation and the reputation of our investment strategies may be negatively impacted.

We may enter into new lines of business, make strategic investments or acquisitions or enter into joint ventures, each of which may result in additional risks and uncertainties for our business.

Subject to market conditions, we may choose to grow our business through, among other things, (i) increasing assets under management in existing investment strategies, (ii) pursuing new investment strategies, which may be similar or complementary to our existing strategies or be wholly new initiatives, or (iii) consummating acquisitions of other investment advisers or entering into joint ventures.

Making strategic investments or acquisitions and entering into strategic relationships, joint ventures, or new lines of business, involve numerous risks and uncertainties, including those associated with investment of capital and other resources and with combining or integrating operational and management systems and controls and managing potential conflicts. Entry into certain lines of business may subject us to new laws and regulations and may lead to increased litigation and regulatory risk. If a new business generates insufficient revenues, produces investment losses, or if we are unable to efficiently manage our expanded operations, our results of operations will be adversely affected, and our reputation and business may be harmed. In the case of joint ventures, we are subject to additional risks and uncertainties in that we may be dependent upon, and subject to liability, losses or reputational damage relating to, systems, controls and personnel that are not under our control.

We may be unable to successfully execute strategic investments or acquisitions or enter into joint ventures, and we may fail to successfully integrate and operate new investment teams, which could limit our ability to grow assets under management and adversely affect our results of operations.

Although we periodically consider strategic investments or acquisitions as part of our growth strategy, we have not at this time entered into any binding agreements with respect to any strategic investments or acquisitions or any strategic relationships or joint ventures and we cannot assure you that we will actually make any additional acquisitions. Our ability to execute our acquisition strategy will depend on our ability to identify new lines of businesses or new investment teams that meet our investment criteria and to successfully negotiate with the owners/managers who may not wish to give up control of the target fund general partner or managing member, as the case may be. We cannot be certain that we will be successful in finding new investment teams or investing in new lines of business or that they will have favorable operating results following our acquisitions.